For businesses aiming to enhance their cash flow by selling invoices, understanding the distinctions between recourse and non-recourse factoring is a fundamental step. Both options can unlock immediate funding, but the obligations and risks they carry are very different. To make the best decision for your financial wellbeing, it’s vital to know how each type of factoring works and what it means for your bottom line. If you want a deeper dive into the essentials, this detailed discussion of recourse vs non-recourse factoring explains what sets these options apart and how to choose the right one for your business.

Factoring, in simple terms, means selling your accounts receivable to a third party at a discount to receive quick funding. The ability to convert pending invoices into working capital can help meet urgent expenses, fuel growth, and provide operational stability. However, factoring is not a one-size-fits-all solution, and your risk exposure and costs will depend on whether you choose recourse or non-recourse models.

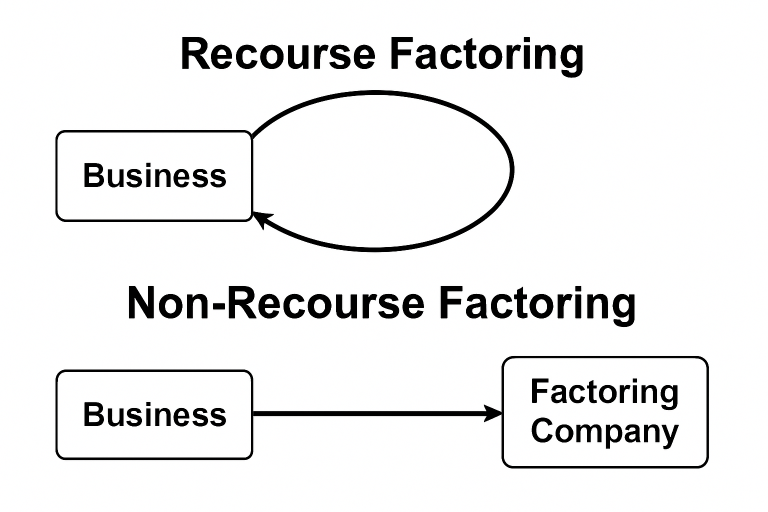

Recourse factoring leaves you responsible if your customer fails to pay, meaning you may need to buy back unpaid invoices or replace them with others. This model typically comes with lower costs and greater accessibility. Non-recourse factoring, on the other hand, transfers certain non-payment risks to the factoring company, usually at a higher price. Non-recourse deals offer more peace of mind but have stricter qualification requirements and may not shield you from every type of default scenario.

By carefully considering these differences, you can create a funding strategy that fits your company’s risk tolerance, client base, and cash flow needs. The right choice can help protect your finances while providing the support your business needs to grow and thrive.

Understanding Invoice Factoring

Invoice factoring is a commonly used financial solution that allows businesses to convert their outstanding invoices into cash by selling them to a factoring company at a discount. This provides almost immediate access to working capital that can be used for various operational needs, such as payroll, purchasing inventory, or investing in growth opportunities. Instead of waiting 30, 60, or 90 days for customer payments, businesses can use factoring to bridge gaps in cash flow and improve liquidity.

Unlike loans or lines of credit, invoice factoring is not based on business creditworthiness alone. Factoring companies mainly consider the payment reliability of your customers, making this option viable for companies with strong customer relationships but limited credit history. According to prominent business sources like Investopedia, this can be especially helpful for young or rapidly expanding companies.

What Is Recourse Factoring?

What Is Recourse Factoring?

Recourse factoring is the most common type of factoring arrangement. Here, if a customer fails to pay an invoice, the business that sold the invoice must buy it back from the factor or provide a substitute invoice of equal value. Because the factoring company faces less risk with this structure, fees are often lower and advance rates are higher. In some cases, the process of approval and funding is also quicker because the focus is primarily on invoice volume and customer quality.

This arrangement suits businesses whose customers generally have reliable payment histories. However, it also means that if an unexpected default occurs, the business must absorb the loss, sometimes requiring substantial reserve funds or credit to manage such contingencies.

What Is Non-Recourse Factoring?

Non-recourse factoring provides protection against customer non-payment, as the risk(under specified conditions)passes to the factoring company. If a customer goes bankrupt or faces other qualifying events that prevent payment, the factor absorbs the loss. Due to the higher risk, non-recourse factoring costs more and can come with lower advance rates. Additionally, the qualification process includes more stringent checks on your customers’ creditworthiness and business standing.

It’s important to note that “non-recourse” may not cover all reasons for non-payment. Often, protection is limited to declared insolvency and does not include payment disputes or invoice issues. For example, an invoice disputed due to quality or service issues is typically not covered by non-recourse agreements. For a more nuanced exploration, Forbes provides valuable context on non-recourse factoring terms and conditions.

Pros and Cons of Recourse Factoring

Pros:

- Lower fees and higher advance rates improve overall cash flow efficiency.

- Approval and funding tend to be faster, supporting urgent financing needs.

- Qualification standards are more flexible, making it accessible to a wider range of businesses.

Cons:

- Business is at risk and must cover defaults on invoices, potentially leading to financial strain.

- Unexpected non-payments can disrupt planning and budget forecasts.

Pros and Cons of Non-Recourse Factoring

Pros:

- Greater peace of mind, since the factoring company assumes defined credit risk.

- Safeguards business stability and supports uninterrupted operations during customer insolvencies.

Cons:

- Higher fees and lower advance rates due to the added risk absorbed by the factor.

- Strict eligibility criteria may exclude some businesses or accounts receivable.

- Non-payment protection is often limited to specific scenarios such as bankruptcy—not payment disputes.

Factors to Consider When Choosing Between Recourse and Non-Recourse Factoring

- Client Creditworthiness: A portfolio of highly reliable, creditworthy customers may suit recourse funding. If some clients pose default risks beyond your control, non-recourse may provide better coverage.

- Risk Tolerance: Some businesses are prepared to accept the responsibility for rare non-payments, while others prioritize peace of mind and operational continuity.

- Cost Considerations: Factoring fees can erode profit margins, so calculate the impact of higher non-recourse rates versus lower recourse rates as you forecast your net gain from factoring.

- Cash Flow Needs: Compare advance rates and funding speed to ensure your chosen model reliably supports your operational requirements.

Conclusion

Selecting between recourse and non-recourse factoring requires a thoughtful evaluation of your clients’ payment histories, your ability to handle risk, and your business’s demand for cash flow certainty. By carefully weighing these factors, you can choose a factoring model that not only improves liquidity but also aligns with your financial priorities and growth ambitions.